Executive summary

The U.S. Small Business Administration (SBA) has initiated termination proceedings against 154 Washington, D.C.-based 8(a) Business Development (BD) Program participants after an internal eligibility review found they no longer met “economic disadvantage” requirements (net worth, adjusted gross income, and/or total assets). [1]

For the firms involved, this is not only a headline—it is a high-stakes administrative process with fast deadlines: a Letter of Intent to Terminate typically triggers a 30‑day response window, and any final termination decision generally must be appealed to SBA’s Office of Hearings and Appeals (OHA) within 45 days. [2]

For the broader market (including subcontractors), this action signals intensified scrutiny of 8(a) eligibility, documentation, and “pass-through” risk—especially in sole-source and other limited-competition awards. [3]

What’s happening and what we know so far

SBA’s February 2026 announcement states it sent letters to 154 D.C.-based 8(a) firms to begin termination proceedings, citing an internal review concluding these firms exceeded economic disadvantage thresholds (net worth, adjusted gross income, and/or total assets). The agency says these firms will be suspended for at least 30 days before final termination. [4]

SBA also reported the group received nearly $1.3 billion in 8(a) contract awards from FY 2021–FY 2024, with nearly $1 billion awarded via sole-source awards. The press release includes examples of firms with reported assets far above the applicable cap (e.g., total assets over $35 million). [5]

Federal News Network added operational detail that matters to contractors: sources told FNN SBA sent three items to affected firms—(1) a suspension letter, (2) a letter of intent to terminate, and (3) an (unsigned) voluntary withdrawal agreement. [6]

Uncertainty to note: SBA’s public release discusses the action in aggregate but does not publish the list of the 154 firms by name. That means many prime and subcontract counterparties may only learn of a partner’s status change through direct communication and/or contracting channels. [7]

Legal and administrative basis for termination

The 8(a) BD Program is governed largely by 13 C.F.R. Part 124, and SBA’s authority to terminate is explicit.

SBA may terminate a participant “for good cause,” and “good cause” expressly includes a failure to maintain eligibility, including when an owner no longer meets the economic disadvantage requirements in 13 C.F.R. § 124.104. [8]

The economic disadvantage thresholds at the heart of this action

Under SBA’s current economic disadvantage regulation, SBA evaluates income, net worth, and total assets—and generally treats exceeding any one threshold as disqualifying:

- Net worth: must be less than $850,000 (with specific exclusions, such as the ownership interest in the applicant/participant and equity in a primary residence). [9]

- Adjusted gross income (AGI): SBA presumes an individual is not economically disadvantaged if AGI averaged over the prior three years exceeds $400,000, though the presumption can be rebutted under certain circumstances. [9]

- Total assets: an individual will generally not be considered economically disadvantaged if the fair market value of all assets exceeds $6.5 million (with limited exclusions). [9]

These specific dollar figures were also reflected in SBA’s inflation-related rulemaking in 2022–2023 (e.g., net worth $750k → $850k; AGI $350k → $400k; assets $6M → $6.5M). [10]

How SBA termination and appeals work in practice

This is the “what to do Monday morning” section—especially for small contractors who need to protect pipeline and performance.

The termination process

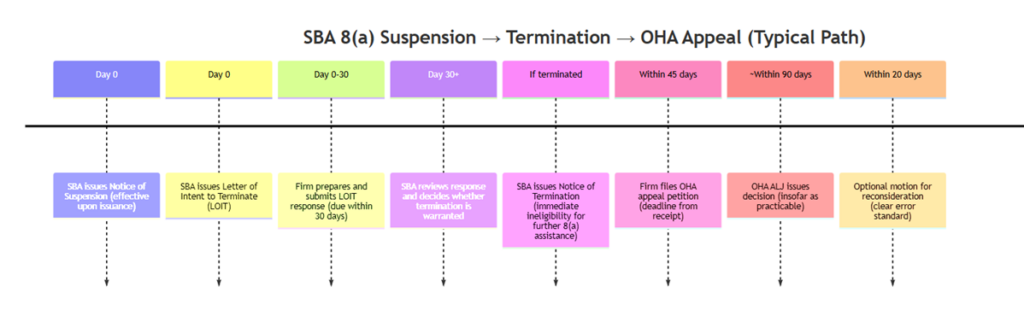

When SBA believes termination is warranted, SBA issues a Letter of Intent to Terminate, which must state the facts/reasons and provide the firm 30 days to submit a written response. [11]

After the response period, SBA reviews the record and may issue a Notice of Termination. Once that notice is issued, the firm becomes immediately ineligible for further 8(a) program assistance (even if it appeals). [11]

Importantly for subcontractors and agency customers: after termination, the firm is generally still obligated to complete previously awarded 8(a) contracts, including priced options that may be exercised. [11]

Suspension during the process

SBA can suspend a participant when needed to protect the government’s interests—including where information shows a clear lack of eligibility. Suspension is effective upon issuance of the notice, and during suspension SBA states that new competitive or sole-source 8(a) awards generally will not be made (unless an agency head determines an award is in the government’s best interest and SBA adopts that determination). [12]

A suspended participant may appeal a suspension to OHA, generally within 45 days, and the suspension remains in effect while the appeal is pending. [13]

Appeals to SBA OHA: deadlines and standard of review

OHA is SBA’s quasi-judicial appellate body. [14]

Key procedural points: * Deadline: an 8(a) appeal petition must be filed within 45 calendar days after receipt of SBA’s determination. [15]

Record-based review: most 8(a) termination appeals are decided solely on the written administrative record, with limited exceptions. [16]

Standard: except in suspension appeals, OHA’s review is limited to whether SBA’s action was arbitrary, capricious, or contrary to law. [16]

Timing: OHA’s administrative law judge issues a decision “insofar as practicable” within 90 days after the appeal petition is filed; reconsideration may be sought within 20 days* for material factual/legal error. [17]

Timeline table: termination and appeal milestones

| Stage | What happens | Typical timing/deadline | Practical implications for small contractors/subs |

| Notice of Suspension | SBA issues suspension notice; limits new 8(a) awards during pendency (with narrow exceptions) | Effective upon issuance/notice | New 8(a) awards may freeze; communicate with teaming partners and COs [12] |

| Letter of Intent to Terminate | SBA states reasons and gives the firm time to respond | 30 days to submit written response | Deadline-driven: gather documents fast; validate SBA’s calculations [18] |

| SBA internal review/decision | SBA considers response and decides whether termination is warranted | No fixed number of days; SBA says it will act “timely” | Uncertainty window; protect pipeline, teaming, and staffing plans [11] |

| Notice of Termination | SBA issues termination notice; firm becomes immediately ineligible for further 8(a) assistance | Effective upon issuance | Existing contracts generally continue; new 8(a) awards stop [11] |

| Appeal to OHA | Firm files appeal petition | Within 45 days of receiving SBA determination | Missed deadline can end the case; calendar immediately [15] |

| OHA decision | ALJ issues final agency decision; binding | “As practicable,” within 90 days after petition filed | Plan for a ~3‑month decision cycle, sometimes longer [17] |

| Motion for reconsideration | Limited reconsideration for clear error | Within 20 days of decision | Rare, but critical if there’s a material mistake [17] |

Mermaid timeline chart: termination/appeal process

Precedent and enforcement context: why this is escalating now

Although the 154-firm action is grounded in economic disadvantage thresholds, it sits inside a much larger enforcement moment.

SBA announced a full-scale audit of the 8(a) program in mid‑2025, stating it would focus first on high-dollar and limited-competition contracts and look back over a long period, with referrals to OIG/DOJ for enforcement where appropriate. [19]

In December 2025, SBA issued letters to all 4,300 8(a) participants requiring extensive documentation (bank statements, financial statements, general ledgers, payroll registers, contracting and subcontracting agreements, and employment records) for the prior three fiscal years—warning noncompliance could result in loss of eligibility. [20]

In January 2026, SBA announced the suspension of 1,091 firms tied to that data call, describing it as roughly 25% of all firms registered in the program. [21]

Outside SBA, Treasury launched a department-wide review (November 2025) of roughly $9 billion in preference-based contracting, explicitly including potential misuse of SBA’s 8(a) program and highlighting “pass-through” arrangements as a suspected abuse pattern. [22]

And oversight around eligibility isn’t new: a GAO report on 8(a) financial thresholds noted SBA assesses economic disadvantage by net worth, total assets, and average income, and recommended SBA evaluate the effects of prior threshold changes. [23] Consistent with that recommendation, SBA later published an evaluation finding the 2020 threshold changes did not significantly affect participation or competition outcomes. [24]

Impacts and compliance lessons for small businesses and subcontracting markets

This action can reshape how small contractors and subs plan bids, teams, and compliance.

Market impacts you may see

First, expect short-term “pipeline turbulence.” When 8(a) firms are suspended, they generally cannot receive new 8(a) awards during the suspension (unless the agency head makes a best-interest determination that SBA adopts). [12] That can delay awards, shift procurements toward competition, or move work to other eligible firms.

Second, expect primes to re-check teaming risk. Even if current work continues, a termination can affect how primes view a partner’s long-term eligibility and may trigger contract/teaming modifications—especially where the 8(a) status was central to the pursuit strategy. [25]

Third, expect more scrutiny of “pass-through” behavior. Treasury’s audit rationale explicitly calls out arrangements where an eligible small business retains fees for minimal participation while subcontracting most work. [22] That focus connects directly to limitations on subcontracting compliance and performance-of-work documentation—especially for service contracts and large IDIQ task orders. [26]

Compliance lessons: protectability comes from paperwork

If your business is in (or works with) the 8(a) ecosystem, treat this as a reminder that eligibility is not “set and forget.” SBA’s rules allow termination for failing to maintain economic disadvantage where required, and also for patterns of failing to provide required submissions/responses (including financial statements and other requested data). [27]

In practical terms, small businesses should assume SBA (and agency partners) will continue requesting and reconciling: * Financials that drive economic disadvantage determinations (net worth, AGI averaging, total assets) and the applicable exclusions/rebuttals. [9]

Ownership/control integrity (because loss of disadvantaged ownership/control is an independent termination basis). [28]

Performance-of-work and subcontracting structures (because awards and oversight are increasingly framed through program integrity and pass-through prevention). [29]

Checklist table: documents to gather immediately

| Category | Documents and data to collect | Why it matters |

| SBA letters and deadlines | Suspension notice, LOIT, any voluntary withdrawal paperwork, proof of receipt dates | Deadlines are short; appeal windows are jurisdictional [30] |

| Owner economic disadvantage file | Personal financial statements, net worth worksheets, documentation of primary residence equity, retirement account restrictions, AGI support (3-year average), explanations for unusual income, reinvestment/tax documentation | Economic disadvantage thresholds and rebuttals are highly technical [31] |

| Firm financial package | 3 years financial statements, general ledgers, bank statements, payroll registers | SBA’s 2025 data call shows what it expects to audit [20] |

| Contracting and subcontracting | Prime contracts, active task orders, subcontracts/teaming agreements, staffing plans, labor category mapping, invoices | Supports performance-of-work narratives and detect “pass-through” exposure [32] |

| Ownership/control evidence | Operating agreements/bylaws, stock ledger/cap table, minutes, officer appointments, compensation records, proof of full-time management | Ownership/control failures are explicit termination grounds [28] |

| Compliance policies and correspondence | Internal compliance memos, prior SBA annual review submissions, correspondence with SBA servicing office | Helps show good-faith reporting and consistent disclosures [33] |

| Past performance / delivery | CPARS inputs, deliverables, performance reports, key personnel resumes | Helps preserve value with customers while legal status is disputed [34] |

Recommended responses for affected firms

If you received one of these letters (or if you are a prime/sub working with an affected firm), consider the following practical steps:

Confirm the math and the definitions. Economic disadvantage calculations are not always intuitive (e.g., specific exclusions exist for net worth; AGI rules include rebuttal concepts; asset valuation is based on fair market value of all assets). [31]

Treat the LOIT response as a “record-building” event. OHA generally decides most 8(a) termination appeals on the administrative record, and the judge focuses on whether SBA’s decision was arbitrary/capricious/contrary to law. Your LOIT response is a core place to build that record. [35]

Calendar the deadlines and preserve proof of receipt. The 30‑day and 45‑day clocks are triggered by receipt, and the OHA filing deadline is strict. [36]

Get specialized counsel early. These are administrative law processes with unique procedural rules (record objections, remand standards, consolidation of suspension/termination proceedings). [37]

Communicate proactively with contracting partners. Even if existing contracts generally continue, suspensions restrict new awards and can create anxiety in prime/sub teams. Clear messaging (status, performance continuity, customer communication plan) can prevent unnecessary off-ramps. [38]

Procura is built for small federal contractors who need to keep moving fast—even when federal contracting rules and enforcement are shifting. Procura is an AI-powered federal contract search and analysis tool that automatically scans SAM.gov, reads full solicitation packages (including attachments), and scores fit against your capability statement—then delivers executive-ready summaries and alerts so you can make smarter bid/no-bid decisions in minutes. [39]

Meet with the Procura Team to See How We Can Help

[1] [4] [5] [7] https://www.sba.gov/article/2026/02/11/sba-moves-terminate-over-150-8a-firms-washington-dc-following-eligibility-review

[2] [11] [18] [25] [36] https://www.ecfr.gov/current/title-13/chapter-I/part-124/subpart-A/subject-group-ECFR3a2020752ea67f7/section-124.304

[3] [19] https://www.sba.gov/article/2025/06/27/administrator-loeffler-orders-full-scale-audit-8a-contracting-program

[6] [30] https://federalnewsnetwork.com/acquisition-policy/2026/02/sba-proposes-to-terminate-154-companies-from-8a-program/

[8] [27] [28] [33] https://www.ecfr.gov/current/title-13/chapter-I/part-124/subpart-A/subject-group-ECFR3a2020752ea67f7/section-124.303

[9] [31] https://www.ecfr.gov/current/title-13/chapter-I/part-124/subpart-A/subject-group-ECFR4ef1291a4a984ab/section-124.104

[10] https://public-inspection.federalregister.gov/2023-15078.pdf

[12] [13] [34] [38] https://www.ecfr.gov/current/title-13/chapter-I/part-124/subpart-A/subject-group-ECFR3a2020752ea67f7/section-124.305

[14] https://www.sba.gov/about-sba/oversight-advocacy/office-hearings-appeals

[15] https://www.ecfr.gov/current/title-13/chapter-I/part-134/subpart-D/section-134.404

[16] [35] [37] https://www.ecfr.gov/current/title-13/chapter-I/part-134/subpart-D/section-134.406

[17] https://www.ecfr.gov/current/title-13/chapter-I/part-134/subpart-D/section-134.409

[20] [32] https://www.sba.gov/article/2025/12/05/sba-orders-all-8a-participants-provide-financial-records

[21] https://www.sba.gov/article/2026/01/28/sba-suspends-over-1000-8a-firms-program-following-december-document-request

[22] [29] https://home.treasury.gov/news/press-releases/sb0309

[23] https://www.gao.gov/assets/d22104512.pdf

[24] https://www.sba.gov/document/report-evaluating-recent-changes-sbas-8a-economic-disadvantage-thresholds